August was another strong month in the Toronto real estate market as sales continued to climb and supply shrinking, buyers are having to pay more money.

The Toronto and surrounding GTA residential real estate market statistics showed August results as anticipated and with results that ensures the market should remain stable overall. The continuing concern though is the lack of supply primarily in the City of Toronto.

The Toronto Real Estate Board (TREB) recently announced that GTA realtors reported 7,711 homes sold in August 2019, an increase of 13.4 per cent compared to 6,797 sales reported in August 2018. On a month-over-month basis, sales were up by 0.8 per cent from July 2019.

“GTA-wide sales were up on a year-over-year basis for all major market segments, with annual rates of sales growth strongest for low-rise home types including detached houses. This reflects the fact that demand for more expensive home types was very low in 2018 and has rebounded to a certain degree in 2019, albeit not back to the record levels experienced in 2016 and the first quarter of 2017. The OSFI mortgage stress test continues to keep some would-be home buyers on the sidelines,” said Mr. Michael Collins, TREB President.

The bulk of the increase in sales volume though was in Toronto’s 905 region. Of the 7,711 reported sales only 2,553 were City of Toronto properties. This number shows little change from the 2,550 sales that took place in the City of Toronto last year. This is mostly due to the average price in the 905 area is approximately 5 per cent less and the lack of properties available to buyers in the City of Toronto.

The average sale price rose 3.6 per cent in the month of August to $792,611 compared to $765,252 for the same period last year. GTA’s home sales have certainly rebounded over the last few months and seem to be adjusting to stricter mortgage-lending rules brought in last year amid higher borrowing costs. The limited housing supply though is driving up prices and sales, as the city’s population continues to grow.

“The GTA’s strong economy, cultural diversity and internationally recognized quality of life continues to attract newcomers to the region each year. This needs to continue for it to remain competitive on the global stage. However, our housing supply has not kept up with population growth, which has led to pent-up housing demand. The province of Ontario, city of Toronto and other GTA municipalities have recognized that housing supply is a key issue and are working toward solutions. With the federal election less than two months away, all political parties should be making their housing policy stance clear as well,” said TREB CEO John DiMichele in a statement.

New listings were down by three per cent year-over-year. TREB says the growth in sales has well-outstripped growth in new listings, which is why overall active listings counted at the end of August were down by more than 11 per cent compared to August 2018.

“This year’s market through August has been characterized by receding listings and increasing sales relative to 2018. Competition between buyers has increased, which has led to stronger annual rates of price growth, most notably during this past spring and summer. Right now, the overall pace of price growth is moderate. However, if demand for ownership housing continues to increase relative to the supply of listings, the annual rate of price growth will accelerate further. This underpins the importance of solving this region’s housing supply issues, which will go a long way to insuring a sustainable pace of price growth over the long term,” said Jason Mercer, TREB’s Chief Market Analyst.

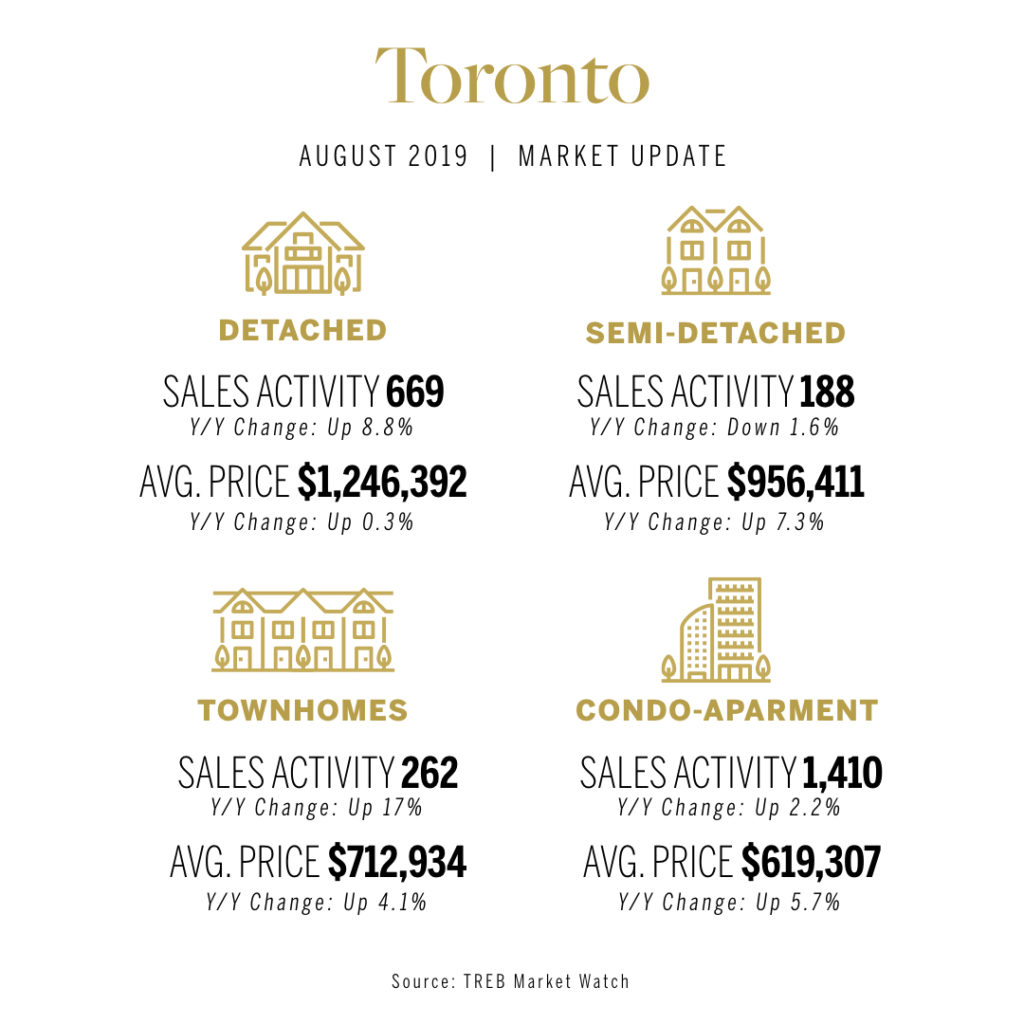

The luxury market also continued its slow rebound. In August, 159 properties having a sale price of $2 Million or higher were reported sold. This is an increase of 10 per cent over the same time last year with 144 reported sold. This sector is still correcting from the inflated prices of 2016 and early 2017, however it is pretty much complete. In the City of Toronto, the average sale price of a detached house in August was $1,246,392 which is an increase of 0.3 percent compared to last year.

The Bank of Canada has held interest rates and with the recent economic numbers including the strength of our labour market, all indications show the GTA residential real estate market will remain stable for the remainder of 2019 and into the start of 2020 with modest gains in sales volume coupled with price increases of approximately 3.5 per cent overall.